How Car Lease Payments are Calculated

We’ve already discussed the separate factors that contribute to the cost of car leasing: net cap cost, cap cost reductions, residual, money factor, and term (see How Leasing Works). Now, let’s put it all together and see exactly how a monthly lease payment is calculated.

It’s easy when you understand how it works.

The “secret” lease payment formula described below is used by dealers and lease financing companies, who would prefer that you not know about it. Even federal leasing regulations do not require that dealers and leasing companies actually disclose how your payment is calculated. The calculation doesn’t appear anywhere on a car lease contract form. There is no way to “check the math” unless you know the formula or have a business calculator.

The result is that the vast majority of people who lease do not know how to check dealers’ math on their lease contract and cannot detect the existence of simple errors, intentional “mistakes”, or out-and-out fraud.

Lack of knowledge of how monthly lease payments are calculated is one of the key reasons that consumers are paying too much for car leases today

Importance of Knowing How to Do Lease Payment Calculation

Let’s establish why it’s so important for you to know how to calculate monthly car lease payments. Consider the following:

- If a dealer figures your lease payment based on full sticker price rather than the discounted price you negotiated with him, how will you know?

- If a dealer doesn’t give you proper credit for your trade-in, even though it’s in your contract, how will you know?

- If a dealer adds hidden charges and fees to your lease without mentioning them or showing them in your contract, how will you know?

- If a dealer mistakenly “drops” a zero and gives you credit for only $100 of a $1000 rebate, even though your contract shows the $1000 rebate, how will you know?

- If a dealer doesn’t account for your $3000 cash down payment in his payment calculation, how will you know?

- If a dealer “bumps” the interest rate (money factor) that he has quoted you (money factor is not shown in lease contracts), how will you know?

Remember, all you see shown on a lease contract is a “bottom-line” monthly payment figure, after the calculations have been done by the dealer in the back office. Therefore, you must be able to check a dealer’s lease payment figures to make sure there are no “mistakes,” intentional or otherwise.

“When I went to pick up the car, the dealer’s calculations seemed wrong. The financial guy reassured me everything was fine. When I demanded to look at their work sheet I saw they had made an “error” on the money rate and also had somehow added some funds to the initial cap cost. In essence, I had been overcharged $75/month. It was corrected … with an apology.”Brenda - Palm Beach, FL

If your payment figures and the dealer’s don’t agree, the only possible reason is that he’s using a different set of numbers for cap cost, residual, money factor, or term than the numbers he’s given you. Ask him to give you exactly the numbers he’s using — and you should be able to exactly match his results, to the penny.

Calculating Monthly Lease Payments — Options

Let’s now look at the lease payment formula — the way that all car leases are calculated. You can use the formula and calculate monthly payments with a simple pocket calculator.

If you don’t particularly like math, our Lease Kit provides easy to use Lease Payment Tables that can be printed and used in place of the formula. The printed tables can be carried with you to the dealer’s showroom so that you don’t need to remember how to do the math there.

Further, our online Lease Calculator does all the math for you. Simply plug in the numbers and get your answer immediately. If you have a smartphone and can access our web site on the Internet, you can use the online calculator right in the dealer’s office to check his calculations.

Monthly Lease Payment Formula

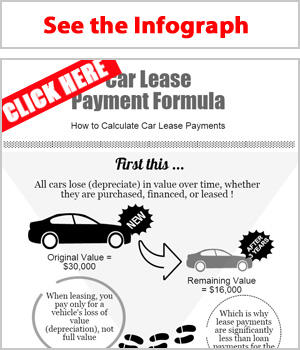

A lease payment is made up of three parts: a Depreciation Fee, a Finance Fee, and Sales Tax — all added together. We’ll look at the first two parts of the formula below. Sales tax is covered a little later.

Depreciation Fee

The depreciation fee portion of your payment simply pays the leasing company for the loss in value of its car, spread over the lease term (number of months), based on the miles you intend to drive and the time you intend to keep the car. You pay off an equal portion of the total expected depreciation each month. This is calculated as follows:

Depreciation Fee = ( Net Cap Cost – Residual ) ÷ Term

Remember, Net Cap Cost is Gross Cap Cost (selling price you negotiate with the dealer) plus any add-on dealer fees and taxes that will not be paid up-front in cash, plus any prior loan balances, minus any Cap Cost Reductions (down payment, trade-in, or rebates). Net Cap Cost does not include any lease charges that you will pay in cash at the time of your lease signing.

Residual is lease-end resale or residual value (as provided by your dealer), and Term is the length of your lease in months.

A good lease deal is when you have the lowest possible Net Cap Cost with the highest possible Residual, along with the lowest possible Money Factor.

Finance Fee

The finance fee portion of your monthly lease payment is like interest on a loan and pays the leasing company for the use of their money. It’s calculated as follows:

Finance Fee = ( Net Cap Cost + Residual ) × Money Factor

Yes, you add Net Cap Cost and Residual — this is not a mistake. It’s not double-counting as it may appear. It’s simply a way of calculating the average amount financed without using complicated constant-yield annuity business formulas (for more details, click here). This is the method used by all lease companies and dealers.

Also be aware that you’re paying finance charges on both the depreciation and residual (the total of which is the negotiated selling price of the car). Remember, you’re tying up the leasing company’s money while you’re driving their car. They used their money to buy the car that you will drive while you lease. Technically, you’re paying finance charges on half of the depreciation (the average value) and all of the residual value for the term of the lease.

The finance fee that you pay with a car lease depends on your credit score. The higher your score, the lower the fee, and the lower your monthly payment. You should always know your latest FICO credit score before going shopping for a car lease or loan. Get a Dark Web Scan and your Experian Credit Report for FREE!

What About Interest Rate?

You won’t find your Monthly Finance Fee or Interest Rate or Lease Money Factor shown in your lease contract. It’s not required by law. Rather, they only show you a “Lease Charge” or “Rent Charge,” which is the sum of all your monthly finance fees over the entire term of your lease. So, to find your Monthly Finance Fee when you only know your “Lease Charge” (or “Rent Charge”) use the following formula:

Monthly Finance Fee = Lease Charge ÷ Term

— or —

If you know your “Lease Charge” or “Rent Charge” from your lease contract and you want to know your Money Factor, use the following formula:

Money Factor = Lease Charge ÷ ( (Net Cap Cost + Residual) x Term )

— then —

To convert Money Factor to APR Interest Rate, use the following formula:

Interest Rate = Money Factor x 2400

or use our

Total Monthly Payment

Now, add the Depreciation Fee and the Finance Fee that you calculated above to get your Total Monthly Payment.

Sales tax must also be added in most states, but we’ll hold that discussion until later.

Total Monthly Payment = Depreciation Fee + Finance Fee

Example Calculation Using the Leasing Formula

So now that we’ve looked at the car lease payment formula, let’s see how it actually works.

Let’s assume you’ve decided on 3-year (36 month term) lease of a Toyota Camry XLE that has a sticker price of $24,600 (MSRP).

You have managed to negotiate the price down to $23,000 (Cap Cost). You decide not to make a down payment, but you have a trade-in worth $5000. Your Net Cap Cost is therefore $23,000 – $5000 = $18,000.

Now, the dealer tells you (because you asked) that the Money Factor is .00375 (.00375 x 2400 = 9.0%) and the Residual Percentage is 60% of MSRP. So your Residual amount, in dollars, is .60 x $24,600 = $14,760.

Now let’s do the math:

Depreciation Fee = ( $18,000 – $14,760 ) ÷ 36 = $90.00

Finance Fee = ( $18,000 + $14,760 ) × .00375 = $122.85

—

Monthly Lease Payment = $90.00 + $122.85 = $212.85 (sales tax not included)

Summary

The lease payment formula is not complicated and can be used on a common pocket calculator. However, if you’re not comfortable with performing the math, especially under pressure in a dealer’s showroom, you can use the easy Payment Tables contained in our optional Lease Kit.

Or if you’ve already leased and need to know if your deal was fair and honest, use the Lease Inspector in our optional Lease Kit.

Or you can use our Lease Payment Calculator to calculate payments. Or use our Lease vs Buy Calculator to compare lease versus loan costs.

Other Ways to Learn About the Lease Payment Formula

Please read the next section, Lease Taxes and Fees.