Which is Better: Leasing a Car or Buying a Car?

The answer is — it depends. It’s not possible to simply say that one is always better than the other because the answer depends on the specifics of each individual situation, which we will explain further.

Leasing a car is a great option for some people, but not for others. Some will not qualify because of credit, income, or other requirements. Therefore, if you are considering leasing, it’s important to know how to determine if a lease is a good option for you, or if you qualify.

Lease vs Buy: The Basics

First, leasing is only an option for financing brand new cars, not used cars, although leasing of used luxury cars is available from specialty car dealers in some cities.

Leases and purchase loans are simply two different methods of automobile financing. Car leasing is not renting as many people seem to think. It’s not at all like apartment leasing. Although leasing is similar to renting in some respects, car leasing and car renting are completely different and should not be confused.

Ask Yourself These Questions

- Which is more important: Driving a new vehicle every two or three years with no major repair risks — or driving one vehicle for many years and assuming responsibility for all maintenance repairs after the first years?

- Which is more important: Lower monthly payments but higher long term cost — or lower long-term cost but higher initial monthly payments?

- Which is more important: Building ownership value and paying off your vehicle, even though it means higher monthly payments — or building no ownership value, with the benefit of significantly lower monthly payments?

- Do you drive no more than an “average” amount of miles in a year — or is your mileage highly unpredictable?

- Do you take good care of your cars and maintain them properly — or do you prefer be more lax about such things?

- Do you have a stable lifestyle such that you will not want to end your lease early — or is there a high likelihood of wanting out early?

So we find out that making a lease-or-buy decision is not quite cut-and-dry. There are trade-offs, pluses and minuses, and pros and cons to consider.

Let’s look at how leasing and buying compare.

Buying and Leasing Compared

Lease

When you lease, you pay only a portion of a vehicle’s total value, which is the part of the value that you “use up” during the time you’re driving it.

You have a choice of not making a down payment, you pay sales tax only on your monthly payments (in most states), and you pay a financial rate, called money factor, that is similar to the interest on a loan. You may also be required to pay fees and possibly a security deposit that you don’t pay when you buy.

You make your first payment at the time you sign your contract — for the month ahead. Your next payment is due a month later. At lease-end, you may either return the vehicle, or purchase it for the part of the value that you haven’t already paid. The purchase price is stated in your contract at the time you sign.

If you decide to return your vehicle, you may be charged a lease-end disposition fee, and for any excessive mileage or wear-and-tear, the details of which are spelled out in your lease contract. Purchasing your vehicle avoids these fees.

Buy

When you buy, you pay for the entire value of a vehicle, regardless of how many miles you drive it or how long you keep it. You can pay cash or get an auto finance loan.

Monthly loan payments are always higher for a loan than for a lease — 60%-110% higher — for the same car. You typically make a down payment of 10%-20%, pay sales tax on the full purchase price, and pay a loan interest rate determined by your loan company, based on your credit score. You make your first payment a month after you sign your contract.

Later, you may decide to sell or trade the vehicle for its depreciated resale or trade value, which may be considerably less than the vehicle’s original cost. The feasibility of selling or trading before loan completion depends on your equity — your vehicle’s current value versus your outstanding loan balance. If the loan balance is higher, you have negative equity — not good. Otherwise, you have positive equity — good.

Lease Example

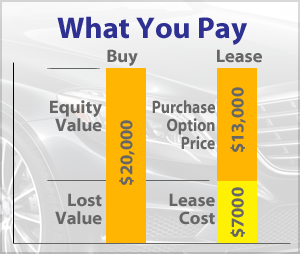

If you lease a $20,000 car that will have, say, an estimated resale value of $13,000 after 24 months, you only pay for the $7000 difference (the depreciation), plus finance charges. This is fundamentally why leasing offers significantly lower monthly payments. You can return the car at lease-end, or buy it for the remaining $13,000 that you haven’t already paid — or trade it if the vehicle is worth more than $13,000.

If you lease a $20,000 car that will have, say, an estimated resale value of $13,000 after 24 months, you only pay for the $7000 difference (the depreciation), plus finance charges. This is fundamentally why leasing offers significantly lower monthly payments. You can return the car at lease-end, or buy it for the remaining $13,000 that you haven’t already paid — or trade it if the vehicle is worth more than $13,000.

Buy Example

When you buy with a loan, you pay the entire $20,000 cost, plus finance charges. You own the car at the end of the loan, although its value is less than the $20,000 you initially paid — $7000 less. All cars suffer the same value depreciation regardless of how they are financed — purchase or lease. You have the option to sell or trade the vehicle, or continue driving it while enjoying no further monthly payments.

How are Car Lease and Loan Payments Different?

Here’s a table that compares a typical lease payment with loan payments for the same car, same price, same down payment, same interest rate, and same number of months. Lease payments are 42% less. An additional comparison shows that lease payments are still lower by 36% even when compared to a 0% loan interest rate.

|

Lease vs Loan Typical lease payment compared to a 0% loan and 6% loan. Do your own comparisons using our Lease vs Buy Calculator

|

Lease Payments – Two Parts

Lease payments are made up of two parts: a depreciation charge and a finance charge. The depreciation part of each monthly payment compensates the leasing company for the portion of the vehicle’s value that is lost during your lease ($7000 in our example above). The finance part (called money factor) is interest on the money the lease company has tied up in the car while you’re driving it. In effect, you are borrowing the money that the lease company used to buy the car from the dealer. You repay part of that money in monthly payments, and repay the remainder when you either buy or return the vehicle at lease-end.

Since you pay only for a leased car’s depreciation (lost value), you have nothing to show for the money you’ve spent. But, as we’ll see in a moment, a car buyer also loses the same value to depreciation.

Loan Payments – Two Parts

Loan payments also have two parts: a principal charge and a finance charge, similar to lease payments. A finance company, credit union, or bank issues money directly to you or a dealer, and you agree to repay that money, with interest, over time. The principal part pays off the full vehicle purchase price ($20,000 in our example above) over the term of the loan, while the finance part is interest on the monthly unpaid balance. The finance company or bank will hold the vehicle’s legal title of ownership until the loan has been completely repaid.

However, since all vehicles depreciate in value by the same amount regardless of whether they are leased or purchased, part of the principal portion of each loan payment can be considered as a depreciation charge, just like with leasing — it’s part of each monthly payment that you never get back, even if you sell the vehicle in the future. It’s lost money for which you’ll have nothing to show, just like with leasing.

The Part You Lose, The Part You Keep

The other part of each loan principal payment, after depreciation, goes toward equity value. Equity is what remains of your car’s original value at the end of the loan after depreciation has taken its toll. Equity is resale or trade value. It’s what you get back if you sell the vehicle — or credit you receive if you trade. The longer you own and drive a vehicle, the less equity value you have. At some point in time, after the wheels have fallen off and the engine is worn out, the only equity left is scrap value. You never get back the full amount you paid for your vehicle.

Savings Account or No Savings Account

So, buying a car with a loan is essentially like putting money into a declining-value savings account — you never get out as much as you put in. A portion of every payment you make is lost to depreciation and finance charges. What you have “to show” for your investment when your loan is paid off is only the part of a vehicle’s value that is left over after depreciation and interest. However, if you plan to drive the vehicle for many years to come, its equity value at the end of your loan is of little concern to you.

Leasing, then, is similar to buying but without the equity “savings account.” You only pay for what you use (the depreciation) and you don’t put anything extra each month into “savings.” It’s true that you’ll own nothing at the end of a lease; you’ll have nothing “to show” for the money you’ve put into it. But … what you don’t own is the same part of the car’s original value — the depreciated part — that a buyer too doesn’t own at the end of his loan. Again, a car’s value depreciates the same amount whether it is leased or purchased. That money is gone forever, lease or buy.

With leasing, you may have the option of putting your monthly payment savings into more productive investments, such as mutual funds or stocks that have the possibility of increasing in value. In fact, many experts encourage this practice as one of the benefits of leasing, although most people will typically find other uses for the money they save by leasing — such as paying the mortgage or buying groceries.

Price is important whether you lease or buy

When leasing, it’s often easy to overlook the fact that vehicle price is important and should be negotiated just as it should if you were buying. In fact dealers sometimes state, or imply, that price is not important or that price cannot be negotiated in a lease. Not true. Just the opposite. Price is the most important factor — in either a lease or a purchase — for creating a low monthly payment.

Get competitive car prices from dealers in your area using our LeaseGuide Car Deal Finder

Leasing Can be a Little More Complicated

Because leasing is made somewhat more complicated with residuals, term, money factors, acquisition fees, etc.; it shouldn’t be undertaken quite as casually as you might with a car loan. There are more opportunities to misunderstand and make mistakes. Therefore, leasing requires that you be more careful and more informed. This is precisely the reason we’ve provided this Lease Guide and our optional Lease Kit — to make leasing as easy and understandable as possible.

Credit Score is Important

Leasing typically requires a higher credit score than buying with an auto loan.

Your score might mean the difference between leasing and buying, what you’ll pay in finance charges, how much down payment you’ll be asked to make, or not getting approved at all.

Get a Dark Web Scan and your Experian Credit Report for FREE!

Insurance Cost Is a Consideration Too

These days, most loan and lease finance companies require you to have full insurance coverage on your car — to protect both your interests and theirs. Since auto insurance companies’ rates for full coverage varies so widely, it’s always a good idea to do some checking around and get quotes.

Leases are More Difficult to Evaluate

It’s easy enough to evaluate a car purchase based simply on price. You can use a free service such as Edmunds.com to compare the price you are being offered to what other people are paying for the same car.

However, evaluating a lease is more difficult because payments are based on a combination of factors, of which price is only one. There’s also residual value, term, and money factor. To help you, we’ve developed an easy-to-use free online Lease Deal Calculator that does the job for you.

One Other Thing – GAP Protection

Most car leases have automatic built-in GAP coverage, while car purchase loans do not. GAP coverage, or GAP insurance, pays the difference between what you owe on your loan or lease, and what your vehicle is actually worth if your vehicle is stolen or destroyed in an accident.

Why is GAP insurance important? Because it’s very common, in these days of long-term loans and leases, rolled-over and refinanced loans, and little or no down payment, to be “upside down” — to owe more on your loan or lease than your car is actually worth.

This can mean you’ll still owe hundreds or thousands of dollars to the finance company even after your insurance has paid for your car that has been totaled or stolen. This turns out to be a huge shocking surprise for most people caught in this unfortunate situation.

So, nearly all leases have built-in GAP protection, but loans do not. You’re better protected with a lease, unless you purchase the insurance separately at extra cost for the loan — if you can find a place to buy it.

So Which is Better – Buying or Leasing ?

As with any question of this type, there can be more than one answer, depending on particulars.

Let’s simplify the answers and summarize them here:

1. The SHORT-TERM monthly cost of leasing is ALWAYS SIGNIFICANTLY LESS than the cost of buying. For the same car, same price, same term, and same down payment, monthly lease payments will always be 30%-60% lower than loan payments. This is still true even when compared to 0% or low-interest loans (see comparison chart above). For your own real-life comparisons, use this excellent Lease vs. Buy Calculator.

2. The MEDIUM-TERM cost of leasing is ABOUT THE SAME as the cost of buying, assuming the buyer sells/trades his vehicle at loan-end and the leaser returns her vehicle at lease-end. The overall cost of leasing compared to buying, over the same lease/loan term, is approximately the same, assuming the buyer sells or trades the vehicle at the end of the loan. Comparisons sometimes show buying to cost a little less than leasing due to fewer fees, lower total finance costs, and the assumption that a purchased vehicle will return full market value if it is sold or traded at the end of the loan (often a bad assumption, especially if traded). However, when the benefits of wisely investing monthly lease savings are considered, along with sales tax savings (in most states), the net cost of leasing can easily be a bit less than buying. For more details see our article, Lease vs Buy – The Real Math.

3. The LONG-TERM cost of leasing is ALWAYS MORE than the cost of buying, assuming the buyer keeps his vehicle after loan-end. If a buyer keeps his car after the loan has been paid off and drives it for many more years, the cost is spread over a longer term. It doesn’t take rocket science to figure out that the cost of buying one car and driving it for ten years is less expensive than leasing or buying four or five different cars over the same period. Therefore, leasing is always more expensive than long-term buying. If long-term financial cost savings were the most important objective in acquiring a new car, it would always be best to buy the car and drive it for as long as it survives — or until the cost of maintenance and repairs begins to exceed the cost of replacing it. However, many automotive consumers have other more short-term objectives that are more important than long-term cost savings.

Lease or Buy? What’s Important to You? What Are Your Priorities?

It’s personal. All of us have different personal styles, objectives, and priorities — in cars, life, and in finances. Car lease-versus-buy decisions must be made with your own lifestyle and priorities in mind. What’s right for one person can be totally wrong for another.

LEASE – If you enjoy driving a new car every two or three years, want lower monthly payments, like having a car that has the latest safety features and is always under warranty, don’t like trading or selling used cars, don’t care about building ownership equity, have a stable predictable lifestyle, drive an average number of miles, properly maintain your cars, are willing to pay more over the long haul to get these benefits, and understand how leasing works, then you should LEASE.

BUY – If you don’t mind higher monthly payments at first, like owning your cars for more than 2-3 years, prefer to build up some trade-in or resale value (equity), enjoy the idea of having ownership of your car, like paying off your loan and being payment-free for a while, don’t mind the unexpected cost of repairs after warranty has expired, drive more than average miles, prefer to drive your cars for years to spread out the cost, like to customize your cars, or you might have lifestyle or job changes in the near future — then you should BUY.

Another Way to Lease — A Better Cheaper Leasing Alternative

The single best way to drive a late-model car at the lowest possible cost is to take over someone’s existing car lease. It’s less expensive than buying and less expensive than taking out a new lease. You avoid all the up-front hassles, negotiations, and fees.

Why?

Most existing car leases were taken out months ago when car manufacturers were offering incredible money-losing lease deals and very low monthly payments. Many people who took those great lease deals now need to get out after losing a job or suffering other financial distress. Most lease companies allow those leases to be transferred to someone else by simply paying a small transfer fee.

Since the original lessee got a good deal — a deal that may not be possible today — anyone taking over the lease will inherit the same great deal, same low monthly payment, with no money down, no up-front sales tax, and in many cases, a cash incentive from the “seller.”

Summary

To summarize, car leasing is the right answer for people who want to save on monthly automobile costs but who have a stable predictable lifestyle and take good care of their cars. Buying is better for those who drive lots of miles, who like paying off their auto loan and enjoying their car without monthly payments for years to come.

Remember, whether you lease or buy, or take over an existing loan, your current credit score can make the difference between a good deal or bad deal, or no deal at all. Always know your credit score. Get a Dark Web Scan and your Experian Credit Report for FREE! Don’t get surprised by what a dealer knows about you that you don’t know about yourself.

Please read the next section, Car Leasing Pros and Cons.